What is invoice financing?

Invoice financing is a way to borrow money from a third party against the amount due from customers. It can help you improve cash flow and execute payments even if you’re waiting for customers to pay their outstanding balances.

Why does a solution like this exist?

We surveyed 1,000 CEOs, founders, directors and senior management and found that at any given time, SMEs are likely chasing £8,500 in outstanding payments. And people who are self-employed are often chasing almost £1,000.

Disruption to cash flow is felt by all business types, but small businesses and start-ups are especially vulnerable. Small businesses are already working with tight budgets, so late payments can:

- Jeopardise your ability to pay employees

- Prevent you from restocking items

- Cause delays in paying your own invoices and expenses

- Blockade your growth

There are generally two ways to quickly inject more cash flow into your business:

- Apply for a business finance loan

- Finance your invoices

In this article, we’ll discuss what invoice financing is, how it works and the differences between a business loan and invoice finance. We’ll also outline the types of invoice financing available to small business owners, how to apply, and the costs and benefits involved.

Table of contents

- What is invoice financing?

- The benefits of invoice financing

- Types of invoice financing

- How invoice financing works and how to apply

- How much does invoice financing cost?

- When to consider invoice financing

- Wrapping up

What is invoice financing?

Invoice financing, also known as accounts receivable financing, is an asset-based financing solution that allows businesses to immediately acquire cash by selling their outstanding invoices or accounts receivable to invoice finance companies for a fee.

For example, an invoice financing firm might lend you 95% of your invoice value and then reach out to your clients themselves to collect payments.

The lender will act as the owner of your invoices and remove the need to chase your clients for payment. Once the client makes their payment, the lender will deduct a fee and release your remaining balance.

Top Tip: If you follow an effective system for creating and following up with invoices, you might not need to approach any invoice finance companies at all. To learn more about invoicing basics and how to avoid common invoice mistakes, read our in-depth guide on how to create an invoice and get paid quickly 💡

Invoice financing is a great option for businesses that don’t want unpaid invoices to affect their cash flow and are looking for a viable alternative to applying for a loan (we’ll dive into why in the next section).

The benefits of invoice financing

Invoice financing is a quick and affordable way to acquire the funds you need to grow your business.

Here are some top benefits of invoice financing for small businesses:

1. Maintain a healthy cash flow

Invoice financing helps businesses get immediate access to working capital that can be used for various purposes, such as:

- Settling any outstanding payments to suppliers

- Paying employee wages on time

- Pursuing a time-sensitive business opportunity

- Acquiring extra inventory

- Expanding your business

Typically, an invoice financing firm hands over 80-95% of your invoice amount. This gives you both immediate access to cash and more control over business decisions, as you no longer need to wait for clients to settle their due payments.

Invoice financing is easier and faster to acquire than a loan

When it comes to eligibility, working with an invoice financing firm is very different from getting a loan approved.

While banks may look at your credit history, business credit score, and financial background to approve a loan, invoice financing companies are primarily concerned with your client’s risk profile.

For example, if your client has a history of delaying payments, the invoice financing firm may charge you a higher fee or refuse to work with you altogether.

In general, the wait time for invoice financing is considerably low, and the approval rate is much higher than traditional bank loans.

Also, traditional loans usually incur a monthly interest expense, while most invoice financing firms only charge a one-time fee.

All of this helps you maintain a steady cash flow for your business so you can continue to grow your company and make critical decisions without worrying about funds.

Top Tip: Maintaining a healthy cash flow is critical to your business’s survival and growth rate. And a cash flow forecast is the best way to keep a pulse on your income and expenses and make strategic decisions. To learn more, read our guide on how to create a cash flow forecast 🔍

2. Save valuable time and resources

Chasing invoices can be both time-consuming and expensive; some businesses might even need to hire a dedicated employee to carry out the task of following up.

Invoice financing eliminates this time and financial expense by taking over the responsibility of running after your clients.

By outsourcing the task of collecting payments, you can focus your resources on more important things, such as maximising sales, improving business operations, creating future strategies and more.

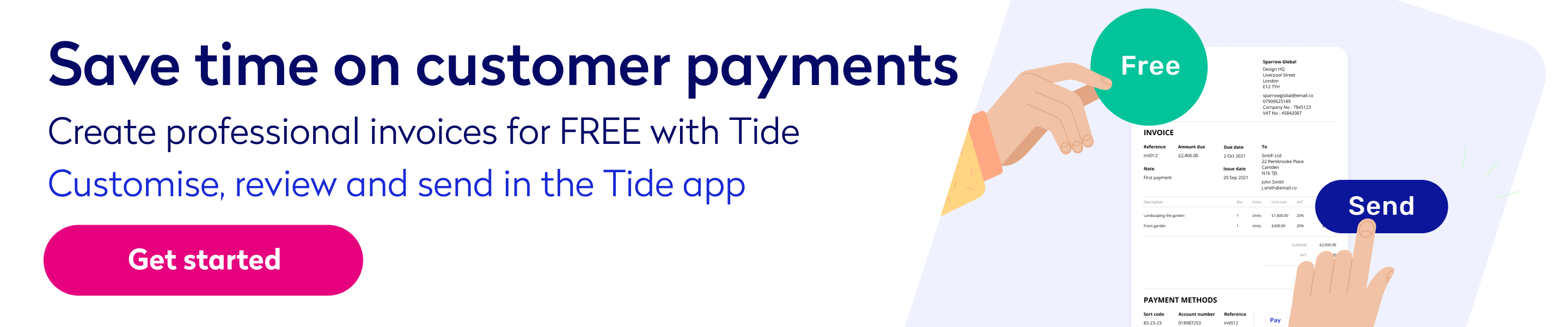

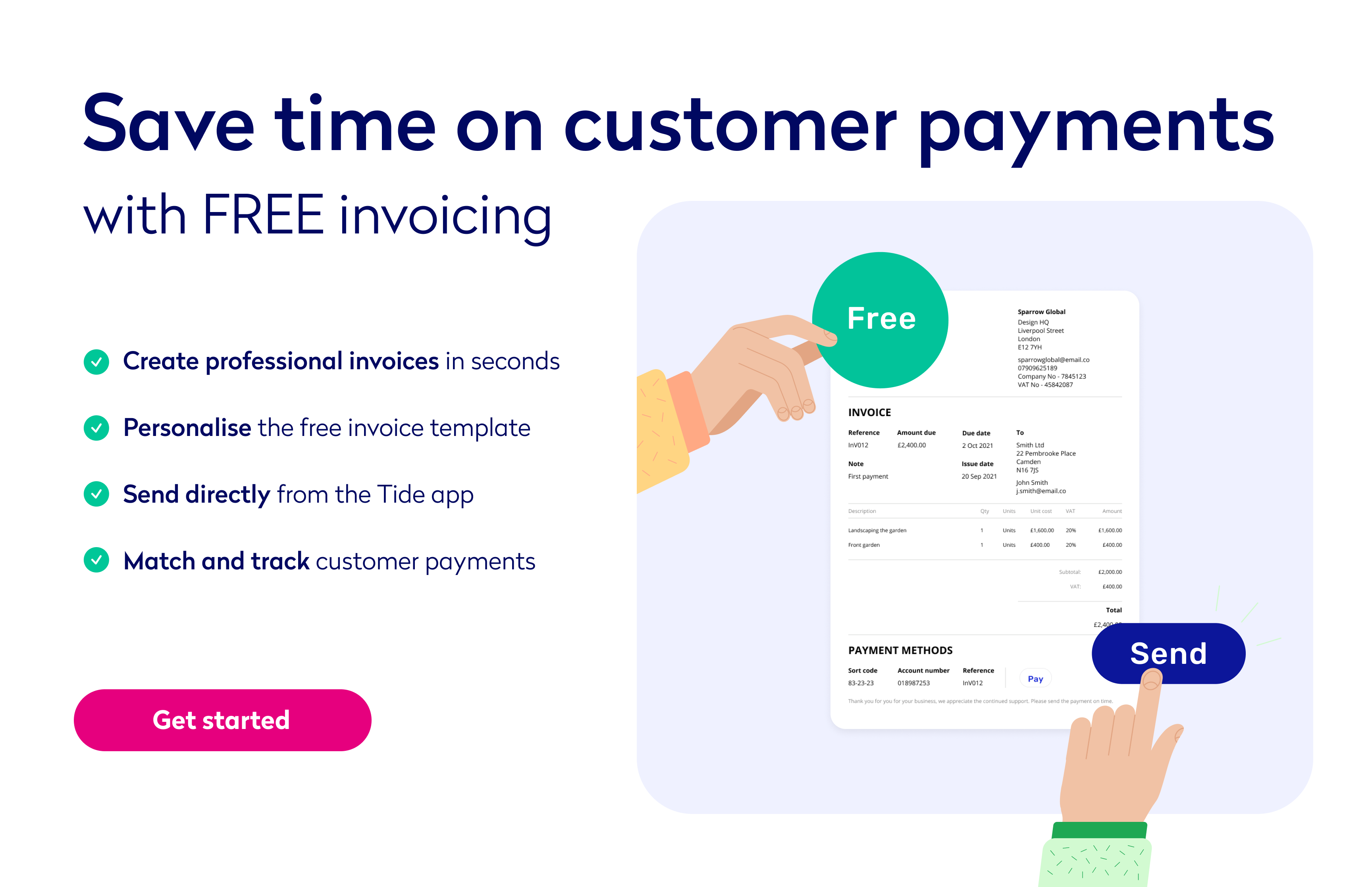

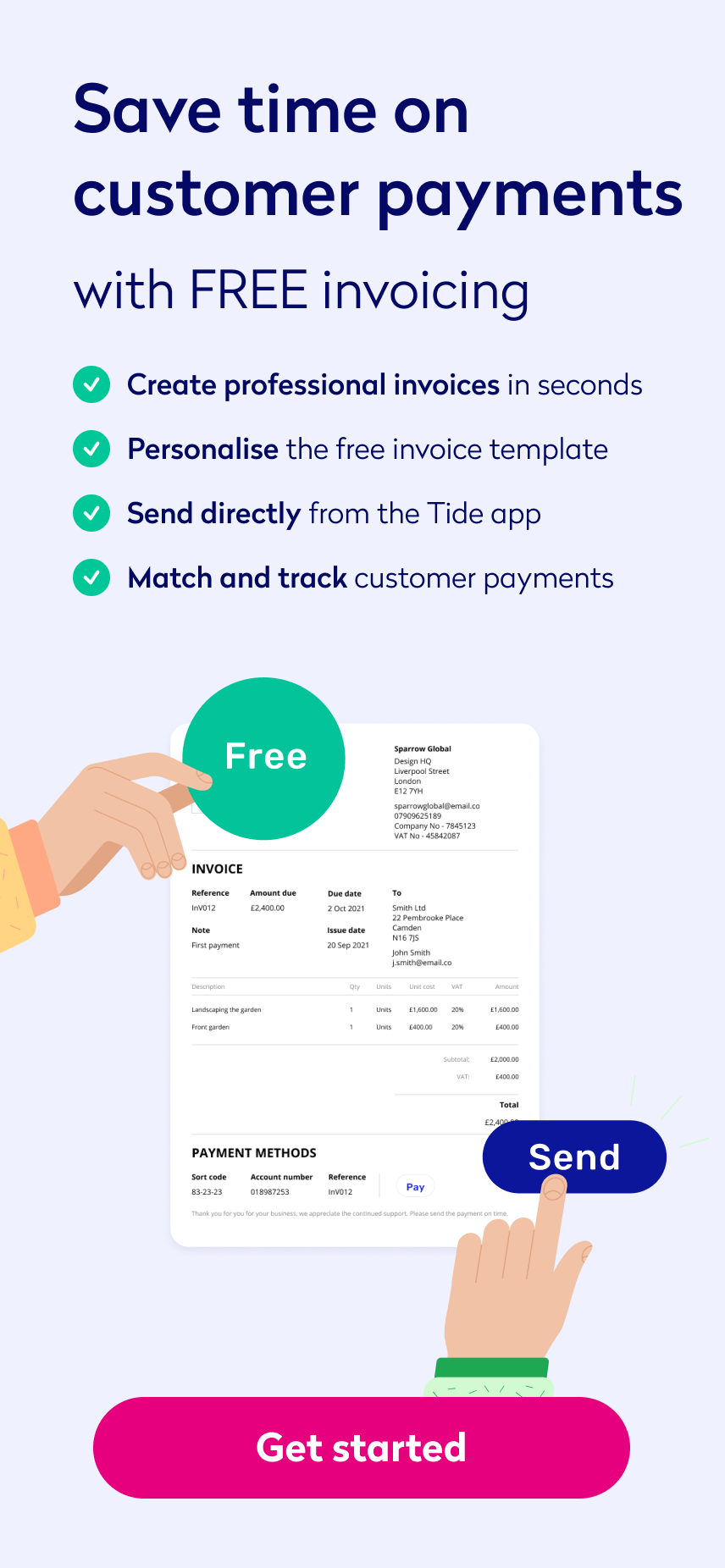

You can also use a tool like Tide invoicing to create, send, and automatically track, follow up, and record payments. It’s as easy as turning on the invoice chaser and choosing a date to follow up. Once it’s paid, Tide will automatically match the payment to the corresponding invoice for you 🔥

3. Build better relationships with clients and suppliers

Getting your invoice financed means you’ll have enough capital to pay your suppliers on time, regardless of payment delays.

Your business’s reliability will help you maintain a good reputation with your suppliers. With a solid relationship, they’ll be more likely to continue doing business with you and come to you with offers.

Invoice financing can also help you build better relationships with your clients. When clients are having difficulty paying, they will appreciate you for offering them an extended credit term, and you’ll still get paid on time.

4. Get protection against non-payment

Another key benefit of invoice financing is that when you outsource the responsibility of collecting payments to a lender, you also protect yourself from non-payment in the process.

Most invoice finance facilities take full responsibility for chasing down your invoices. So, if a client fails to pay, you won’t be as severely affected.

In most cases, the invoice finance facility will bear the losses of an unpaid invoice. The only money you’ll lose will be the amount that was initially withheld by the lending firm.

Protection against late or non-payment on invoices is particularly helpful for small businesses that can’t afford to have a lot of bad debts.

Types of invoice financing

There are several different types of invoice finance options available. The invoice finance solution you choose will depend on your business needs and objectives.

1. Invoice factoring

Invoice factoring is the most popular type of invoice financing available to all businesses.

With invoice factoring, businesses sell their invoices to factoring companies in return for cash received upfront. The factoring firm will then take over the process of chasing down the invoices and collecting payments from your clients.

The amount you receive may vary depending on how risky your invoices are. Typically, invoice factoring firms will pay you anywhere between 80-95% of your total invoice amount in advance.

It’s important to note that invoice factoring agreements require you to inform your clients that you’ve factored your invoices to a third party. This may or may not impact your relationships and future business dealings with those clients.

The two main types of invoice factoring

There are two main invoice factoring types: recourse invoice factoring and non-recourse invoice factoring. Let’s explore both in detail.

Recourse invoice factoring

In recourse invoice factoring, the financing firm holds the responsibility for chasing down invoices and collecting payments from a business’s clients.

However, recourse factoring doesn’t come with bad debt protection. If a client refuses to pay, the business will need to buy its invoice back from the factoring firm. So, in case of any non-payment, the business will bear the full risk.

This type of invoice factoring is more common, and firms will usually offer you a higher amount upfront as the risk involved on their part is very low.

Top Tip: If you’re responsible for collecting payments from clients, make sure you develop an effective follow-up system to remind clients to settle their payments. To learn more, check out this in-depth guide on how to effectively chase invoices without burning bridges 💡

Non-recourse invoice factoring

In non-recourse invoice factoring, the financing firm will be responsible for collecting payments from your clients and bear the full risk in case of non-payment.

Because there is risk involved on the financing firm’s part, they are more likely to give you a lower percentage of your total invoice amount in advance.

When the clients settle their payments, the financing firm will deduct its predetermined fee from the total amount and transfer the remaining balance.

The real bonus with non-recourse invoice factoring is that if a client fails to pay, the financing firm will bear the loss, not the business.

If your invoice is high-risk, meaning there is a high chance the client may not settle their payment, non-recourse invoice factoring might be more suitable than recourse invoice factoring.

Even if you receive less money in advance, it’s still better than not getting paid at all. This is a great way to protect your business from cash flow disruption when you’re dealing with difficult clients.

That said, not many financing firms offer non-recourse invoice factoring. Even if they do, only clients with a good credit rating will be eligible for non-recourse. Additionally, non-recourse options may only be available under special conditions, such as when a client declares bankruptcy.

2. Invoice discounting

Invoice discounting is similar to traditional loans in that the business takes full responsibility for collecting payments from its clients after taking an advance from a financing firm.

Once your client pays you back, you’ll need to return the borrowed amount to the lending firm in full, plus additional charges.

Unlike invoice factoring, the fact that you’re getting your invoice discounted stays hidden from your clients, so it’s less likely to impact your business dealings with them.

Invoice discounting is ideal for larger businesses that have the resources to follow up with clients and chase down outstanding invoices. It’s also a good alternative to invoice factoring if you feel that keeping your clients in the loop might affect your relationship with them.

3. Selective invoice financing

In selective invoice finance, the business chooses which invoices they want to sell or outsource to the financing firm and which ones they want to control themselves.

This method is different from traditional invoice financing options, which usually require you to sell all your accounts receivable to the financing firm.

Selective invoice financing is more flexible than other options. For example, if you’re worried about particular clients or a few large invoices, you can choose to outsource those specifically.

Ideally, you should only outsource potentially risky invoices so you can side-step the hassle of recollection and avoid losing money to financing firms on invoices you can easily collect on your own.

Selective invoice financing is a great option for businesses that want to maintain a steady cash flow and keep their financing costs low at the same time.

4. Spot factoring

Spot factoring allows you to outsource a single invoice from your accounts receivable. Unlike selective invoice financing, you can’t choose to outsource multiple invoices at a time.

The financing firm will work in the same way as it does with traditional invoice factoring. They will take over the payment collection process and pay you back the withheld amount minus the fee once the client pays up.

Spot factoring is usually more expensive than other invoice financing options. It may also negatively impact your client relationships as you’ll need to ask them to send the payment in question to the factoring firm and then resume all future payments in-house.

Furthermore, most financing firms only offer spot factoring for large invoices, so this might not be an ideal option for small businesses or companies that typically deal with smaller, more frequent invoices.

5. Online auction

Another type of invoice financing option is to sell your accounts receivable through online auctions.

Businesses can typically choose the invoice they want to sell and put it up for auction. Investors and lending firms can then analyse the invoice, customer profile and your business before placing their bids.

The person or firm with the highest bid wins full control of your accounts receivable.

How invoice financing works and how to apply

Now that you’re aware of the benefits of invoice financing and the various options you have, let’s talk about the steps involved in getting your invoice financed.

The exact process of invoice financing may vary from business to business, depending on the firm’s unique requirements. Nevertheless, here’s a general overview of what you’ll need to do to set up invoice financing for your business.

Step 1: Enquiry

The process begins by reaching out to the invoice financing firm to inquire about their services and initiate a request.

Before they can approve your request, they will gather information about your company and analyse your operating sector.

The financier may also request information about the following aspects of your business:

- Financials

- Management team

- Key customers

- Trade process

- Invoice details

Depending on the financing firm’s process, they may choose to do this over the phone or in a face-to-face meeting to verify the information.

Step 2: Offer

Once the financier is satisfied with your track record, they’ll draft an offer that typically includes the following:

- The facility requested by your business

- The number of invoices that need financing

- The total amount required as part of the agreement

- Account management costs

- Personal guarantees—a commitment that the agreement will be honoured by both parties

- Terms and conditions

- Further documentation required from the business (if applicable)

Once both parties approve the offer letter, the financier processes the request.

Step 3: Set up

The invoice financier may register a debenture as part of your agreement. Then, they will begin verifying all the invoices you financed, speak to your clients and take care of any disputes that may arise.

Once the audit of your sales ledger is completed, the financier will issue a binding agreement that clearly outlines the costs, terms and conditions, and processes involved in the agreement.

How much does invoice financing cost?

Invoice financing might sound like an easy way to get paid on time, but it can get expensive if you’re dealing with a lot of invoices and clients.

Is invoice financing regulated in the UK?

It’s also important to note that invoice financing is currently unregulated by the FCA (Financial Conduct Authority) in the UK, so the cost quoted by one financing firm might be completely different from the cost quoted by another firm.

Ideally, you should do your research and contact as many financing firms as possible to find the best value for your business.

Once you are satisfied with the information you have on the financing firm, you can then sign an agreement with them.

The most common invoice financing costs

Most invoice financing agreements will involve the following costs:

Service charges

The service charges on your financing agreement will include everything that contributes to managing your account. This could be anything from costs incurred by the lending firm to collect your payments to high-level administrative costs.

The typical service fee for invoice factoring ranges from 0.75% to 2.5% of your total invoice amount.

Service charges for invoice discounting, on the other hand, can be as low as 0.25% of your total invoice amount.

Discount charges

Discount charges are similar to the interest payments you make on a business loan.

These are calculated as a percentage of your invoice value and may increase or decrease depending on how long your clients take to make their payments.

The typical discount charge for an invoice factoring facility is anywhere from 0.5% to 5% of your total invoice amount. This rate is much lower for an invoice discounting facility and doesn’t usually exceed the 3% mark.

The higher the value of your invoice, the lower the discount charge you’ll incur.

Key factors that may directly impact your financing costs

Now that you know about the two main types of costs you’ll incur when dealing with invoice finance providers, let’s discuss some key factors that may directly impact your costs.

- Invoice value: Service charges will be higher for larger invoices and lower for smaller invoices. Discount charges will be higher for smaller invoices and lower for larger invoices.

- Business size: Financing firms prefer doing business with larger companies with a high annual turnover and good credit ratings. If you have a good credit control process in place, your financing costs may be lower.

- Industry type: Some industries are considered low risk, while others are considered high risk. The charges will typically be lower for low-risk industries because the payment collection is usually straightforward and more or less guaranteed. Industries perceived as high-risk, such as labour-intensive industries, may face higher financing charges.

- Client’s credit history: If the invoice you’re outsourcing is sent to a client that has a poor track record of non-payment or late payments, the lending firm may charge a premium for financing that invoice.

When to consider invoice finance

Invoice finance can help businesses of all sizes with better cash flow management and protection against late payments.

However, most invoice finance companies have strict requirements that may or may not apply to your business.

For example, many lending firms require businesses to have a minimum turnover of £50,000 to be eligible for invoice financing.

Additionally, some lending firms require businesses to be a limited company, an SME, or only work with business-to-business (B2B) and not business-to-consumer (B2C) companies.

It’s also common for invoice finance providers to state a minimum invoice value for advance requests, which isn’t always ideal for small businesses.

Before you decide to move forward with invoice financing, it’s a good idea to contact multiple invoice finance companies and see if your business is eligible. Then, do a cost-benefit analysis to assess whether this option is worth it or not. It may make more sense to try to fix your invoicing process in-house first before outsourcing to lending firms.

Top Tip: Before you consider outsourcing invoices to a lending firm, analyse your invoicing process to see if there’s a resolvable issue. Learn more in our step-by-step guide on how to streamline your invoice process💡

Wrapping up

For businesses dealing with late payments and large invoices, invoice financing is a great option to ensure they get the money needed to maintain a healthy cash flow and uninterrupted growth.

Invoice finance is also an excellent alternative to traditional bank loans, as most lending firms are more interested in your clients’ credit histories than yours.

Before you start searching for an invoice finance lender, examine your own invoicing process. You may discover an alternative solution for payment protection.

If invoice financing is your way forward, make sure you do your research to find the best value where you’re most eligible. Then weigh the costs and benefits to see if this option is worthwhile for your business.

Photo by Tim Douglas, published on Pexels